Education Center / The Road Ahead: Opportunities and Obstacles for Heavy-Duty Fueling

Blog

Category: Alternative Fuel, Transportation

The Road Ahead: Opportunities and Obstacles for Heavy-Duty Fueling

It’s no secret that the transportation industry has evolved over the past several years. The introduction of alternative fuels and policies regulating emissions brought with it new opportunities and obstacles that can leave fleets wondering what the best option(s) is for their organization. We will review comparisons, opportunities, and obstacles for each fuel type, specific to heavy-duty vehicles, to help inform fleet owners in their decision-making process.

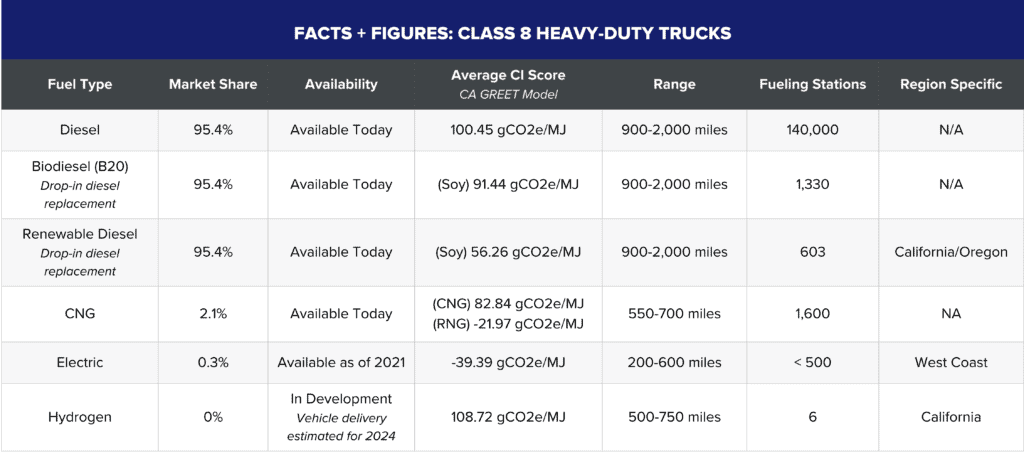

FUEL ASSESSMENT—HOW DO FUELING OPTIONS COMPARE?

Diesel has been the fueling standard for heavy-duty fleets. However, as more options reach commercialization, some question how these alternatives compare both to diesel and one another. In the table below, we answer that question for biodiesel (B20), renewable diesel, compressed natural gas, electric charging, and hydrogen.

Information updated as of October 5, 2023

While vehicle cost is not reported in the above table, it should also be considered. Diesel/biodiesel/renewable diesel currently has the lowest associated vehicle cost with CNG a close second at a ~$30,000-$50,000 mark-up. Conversely, while electric and hydrogen vehicles have higher initial price tags, they also come with the most opportunities to offset costs through grants, region-specific funding, and incentives from programs such as the Inflation Reduction Act.

Policies and regulations also impact vehicle and technology adoption, but both are dependent on region. To determine if there are any fueling types that are required or are restricted in your area, reference local, state, and federal legislation.

OPPORTUNITIES AND OBSTACLES BASED ON YOUR FLEET’S PRIORITIES

No two fleet owners are the same, so we shouldn’t expect a one-size-fits-all approach. Each fleet will have different priorities, meaning what makes a certain fuel type appealing to one, may not matter to another. Below, we’ve outlined four of the most common priorities fleet owners have along with the associated opportunities and obstacles.

1. Market Share + Availability

Diesel/biodiesel/renewable diesel-powered trucks, followed by CNG trucks, currently lead the industry in terms of market share and vehicle availability. These options are great for fleets who are looking for established solutions that have been deployed at scale.

Electric and hydrogen trucks have more considerations due to the newness of the technology. Electric Class 8 trucks have only been available for a couple of years and hydrogen trucks are still early in their trial phase with only a few on the road. A recent partnership between Toyota and PACCAR is expected to accelerate hydrogen vehicle production with initial deployment targets in 2024. More OEMs like Volvo, Peterbilt, Freightliner, and Kenworth are developing and deploying battery electric vehicles (BEVs) and fuel cell electric vehicles (FCEVs), so vehicle availability for both should grow more rapidly in the coming years.

2. CI Score + Emissions

Electric and renewable natural gas (RNG) provide the greatest opportunity for fleets looking to minimize their carbon intensity (CI) score and related emissions. Depending on the feedstock used to produce the electricity and RNG, both fuel types can offer a negative CI score.

Renewable diesel, biodiesel, and CNG all offer slightly improved CI scores when compared to diesel. Hydrogen has the highest CI score of all of these fueling options as over 95% of hydrogen today is produced through natural gas steam reformation. However, efforts to produce cleaner forms of hydrogen from cleaner sources like renewable natural gas or from processes like electrolysis of water are under development. Hydrogen is an attractive option to reduce emissions as it produces zero tailpipe emissions when used as a vehicle fuel, which some states, such as California, will soon be requiring.

3. Vehicle Range

Diesel/biodiesel/renewable diesel-powered trucks provide the greatest vehicle range—aligning with fleets that are looking to go long distances with minimal fuel stops in between.

While CNG, electric, and hydrogen vehicles cannot currently match diesel’s range, original equipment manufacturers (OEMs) and developers are working to extend the range for these technologies. In the meantime, these are great options for fleets running short-haul or return-to-base routes.

4. Fueling Infrastructure Build-Out

Traditional diesel fuel currently has the most established fueling network in the United States. Biodiesel and CNG come in second and third with stations located across the U.S. (and higher concentrations in some areas).

Class 8 accessible renewable diesel, electric, and hydrogen fueling stations are almost all located on the West Coast with the majority falling in California. As more fleets begin to adopt these technologies, we can expect to see additional infrastructure built out along key shipping corridors.

THE ROAD AHEAD—NEXT STEPS

No matter which of the above priorities your fleet aligns with—or which fueling technology you’re looking to adopt—partner selection is key. If you need help evaluating your options or implementing a new fueling type, we’re here to help!